Work with us

The policy that lies behind this legislative proposal is to ensure that the fiscal authorities are made aware of the implementation of any potentially aggressive tax arrangements at an early stage.

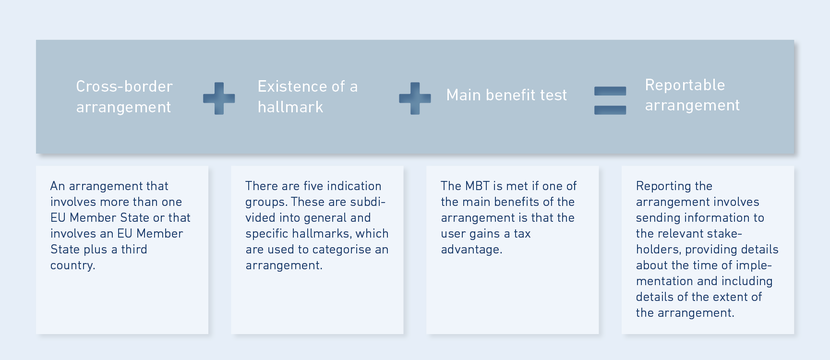

For the time being, the reporting obligation generally applies to tax arrangements subject to taxes which fall under the scope of the Directive on Administrative Cooperation including, in particular, income tax, corporation tax, trade tax, and inheritance and gift tax. VAT is exempt. Please note that some Member States might deviate therefrom and include tax arrangements which are subject to VAT, e.g. currently in Poland or Portugal, into the reporting obligation.

For the purposes of tax compliance, it is advisable to have comprehensive documentation of even those transactions that are not deemed reportable. The content and scope of the data to be transmitted, as well as the sanctions in the event of non-reporting or false reporting, vary from one EU country to another depending on national legislation.

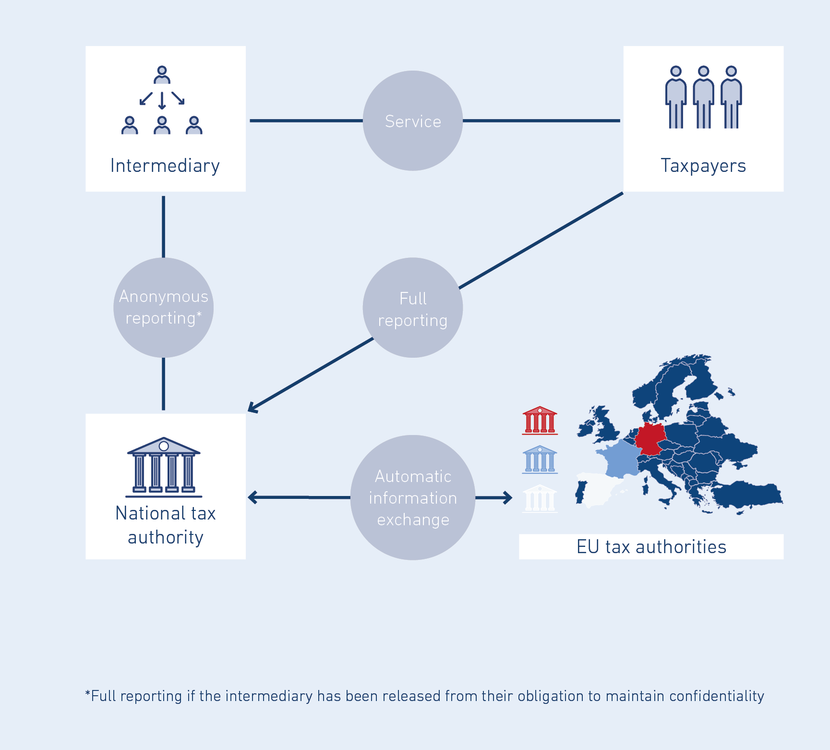

The reporting obligation applies primarily to those known as “intermediaries”. This can be anyone who:

· Is involved in designing and/or implementing the cross-border tax arrangement in an advisory capacity

· Markets the arrangement

· Designs or organizes the arrangement for a third party

· Makes the arrangement available for use or manages its implementation by a third party

The term “intermediary” is not restricted to a specific occupational group; rather it includes the following and more:

· Tax consultants

· Lawyers

· Business consultants

· Representatives of the financial and insurance sector

Where the intermediary is legally obliged to maintain confidentiality, the reporting obligation may be transferred to the relevant taxpayer of the cross-border tax arrangement (art. 8ab para. 5, 6 of the (amended) Directive on Administrative Cooperation). Whether the reporting obligation is allowed to be completely or partly transferred to the relevant taxpayer due to this legal professional privilege depends on the national implementation of the directive by the corresponding Member States.

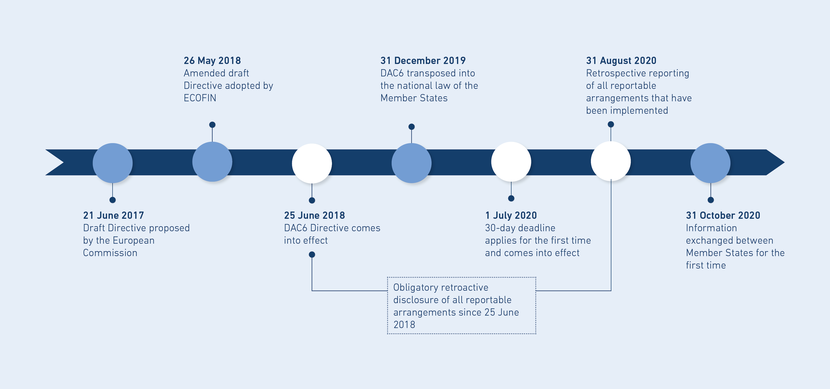

In principle, the report has to be filed within 30 days of the deadline-triggering event specified in art. 8ab para. 1 of the (amended) Directive on Administrative Cooperation.

The reporting deadline applies to all cases in which the deadline-triggering event according to art. 8ab para. 1 of the (amended) Directive on Administrative Cooperation occurs on or after 1 July 2020. In cases where the first step of a reportable cross-border arrangement was implemented between 25 June 2018 and 1 July 2020, the information must be reported by 31 August 2020 (art. 8ab para. 12 of the (amended) Directive on Administrative Cooperation).

As well as retrospectively processing any arrangements you have implemented previously, we also recommend carrying out further preparations by July, firstly by undertaking an impact analysis and secondly by aligning your internal processes – and, in turn, your associated compliance obligations – with the law.

We will be happy to help you with this!

The DAC6 Directive (EU) 2018/822 requires EU Member States to impose compulsory reporting obligations on intermediaries and taxpayers in relation to cross-border tax arrangements. Here you will find all the information you need about the regulatory framework, the challenges involved and our portfolio of DAC6 services.

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.

We use marketing cookies to increase the relevancy of our advertising campaigns.